This 1950s mortgage receipt reveals home payments were cheaper than ordering DoorDash today

Amid high interest rates and ballooning monthly mortgages, a photo of a mortgage payment slip from 1952 has baffled people.

Sept. 16 2024, Published 2:30 p.m. ET

Most aspiring homeowners in America believe that their dream is practically dead. According to a survey conducted by the Harris Poll Thought Leadership and Future Practice, the majority of renters surveyed expressed that areas they live in have become unaffordable. The housing affordability has fallen to its lowest level since the 1980s. Amid high interest rates and ballooning monthly mortgages, a viral post on Reddit, a photo of a mortgage payment slip from 1952, has baffled people.

Here's how much mortgage payments cost in 1952

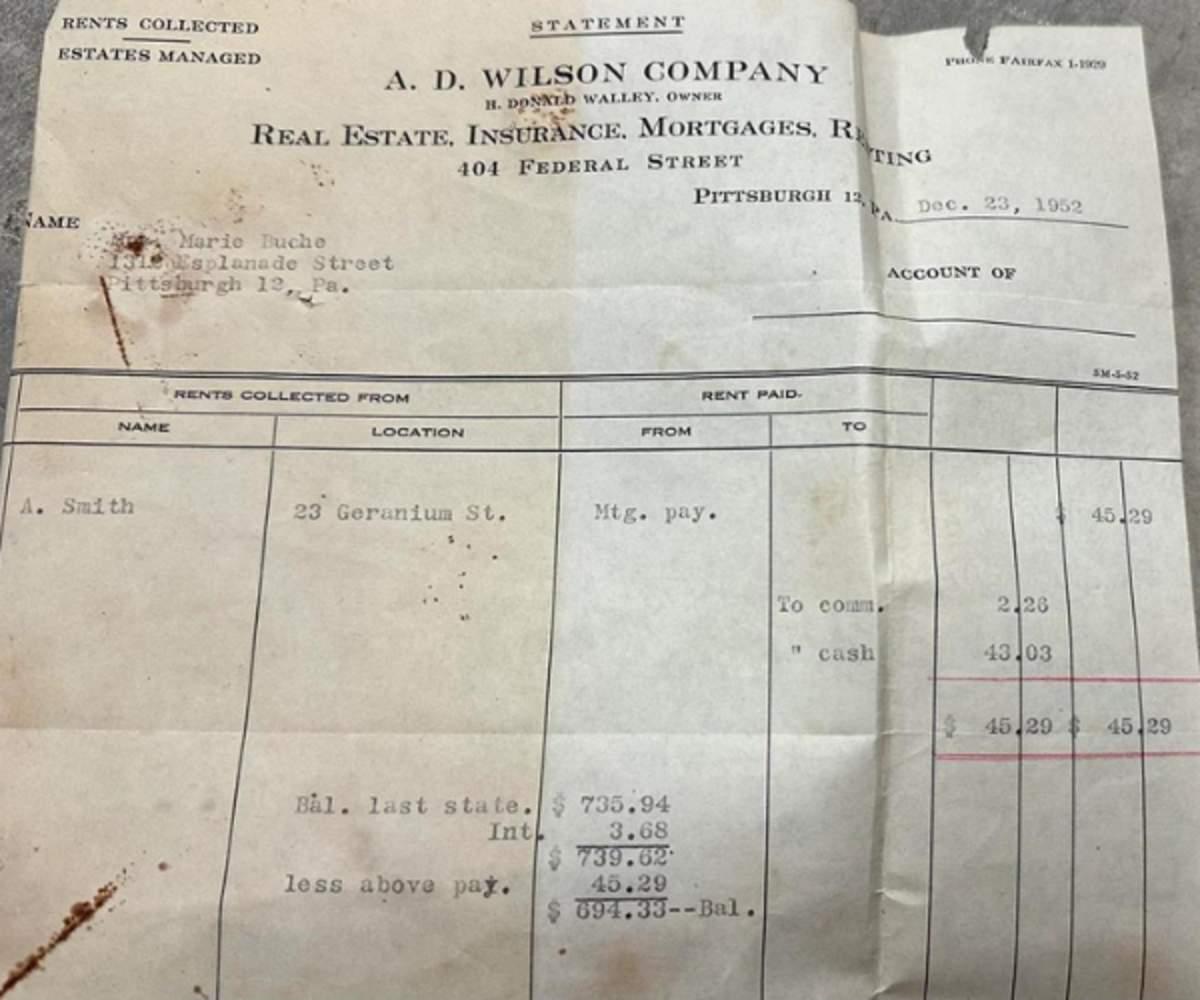

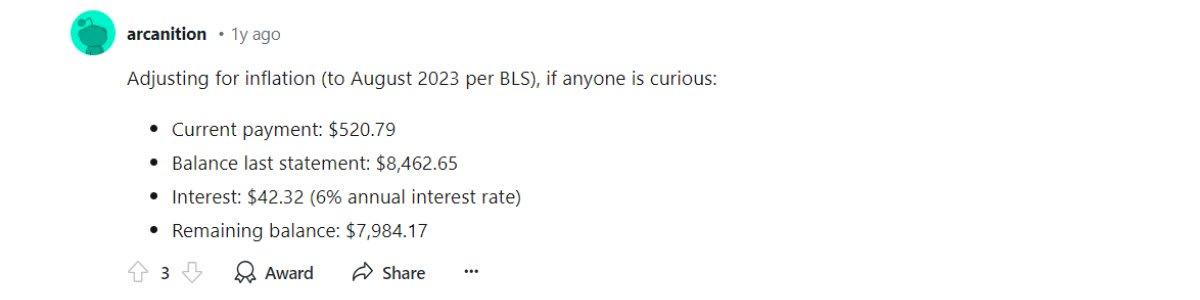

The picture shared by user 1stumbler on the popular forum r/pics shows a payment slip of a property owner in Pennsylvania. As per the document, the person made a monthly payment of merely $45.29 for their mortgage. The average monthly payment on a 30-year mortgage is $2,715 and the same on a 15-year fixed mortgage is $3,552, as per Business Insider's analysis of official data.

Naturally, the post left people baffled and many pulled out their fact books and calculators to prove just how bad the housing market has got. "Census says 1952 median income was $2300. That's a rough monthly of $191.67. So they're paying roughly 24% of their income towards their mortgage," commented u/ravengenesis1.

To this, another user u/day_break added, "This was about 2% of average income a month so 24% overall which is still miles better than our expected 1/3 ratio we have today". The user may be referring to the 28% rule which says no more than 28% of a household's income should go toward mortgage income.

However, another user suggested that even 28% was a distant dream. "My mortgage payment is 2700 dollars. 5X what a normal mortgage was back then," wrote u/Kairukun90. Meanwhile, another user u/kymilovechelle suggested, "Jesus now it costs this much to door dash for one person."

Why is Housing so expensive in America?

There are several factors that make housing extremely expensive in the US. According to a Yahoo Finance report, common citizens are outbid by wealthy investors who pick up inventory, refurbish homes, and put them on the rental market.

The inventory is further cut short by senior homeowners who refuse to downsize. According to an Urban Institute analysis of the 2022 American Community Survey, over half, or 56% of houses with three or more bedrooms are occupied by one or two people, mostly 62 years old or more. This makes finding a comfortable home for young families even tougher.

Furthermore, home buyers also face a mountain of charges to close on a house. These can include "junk fees" in the form of origination fees, credit report fees, discount points, and more. Loans have also become expensive since the pandemic. As per the Consumer Financial Protection Bureau, the median total costs of loans rose by a steep 21.8% just between 2021 and 2022.

In a Forbes report, Lisa Sturtevant, chief economist at Bright MLS, predicted that home prices may ease in late 2024, but housing won't get noticeably cheaper even in 2025.