Here are 5 Financial Scams Pulled off Using Technology That Experts Have Flagged

In 2024, financial scams have escalated, costing U.S. consumers over $7 billion. Advanced technologies like deepfakes are fueling imposter scams.

Feb. 2 2024, Updated 8:37 a.m. ET

The dark side of technological advancement

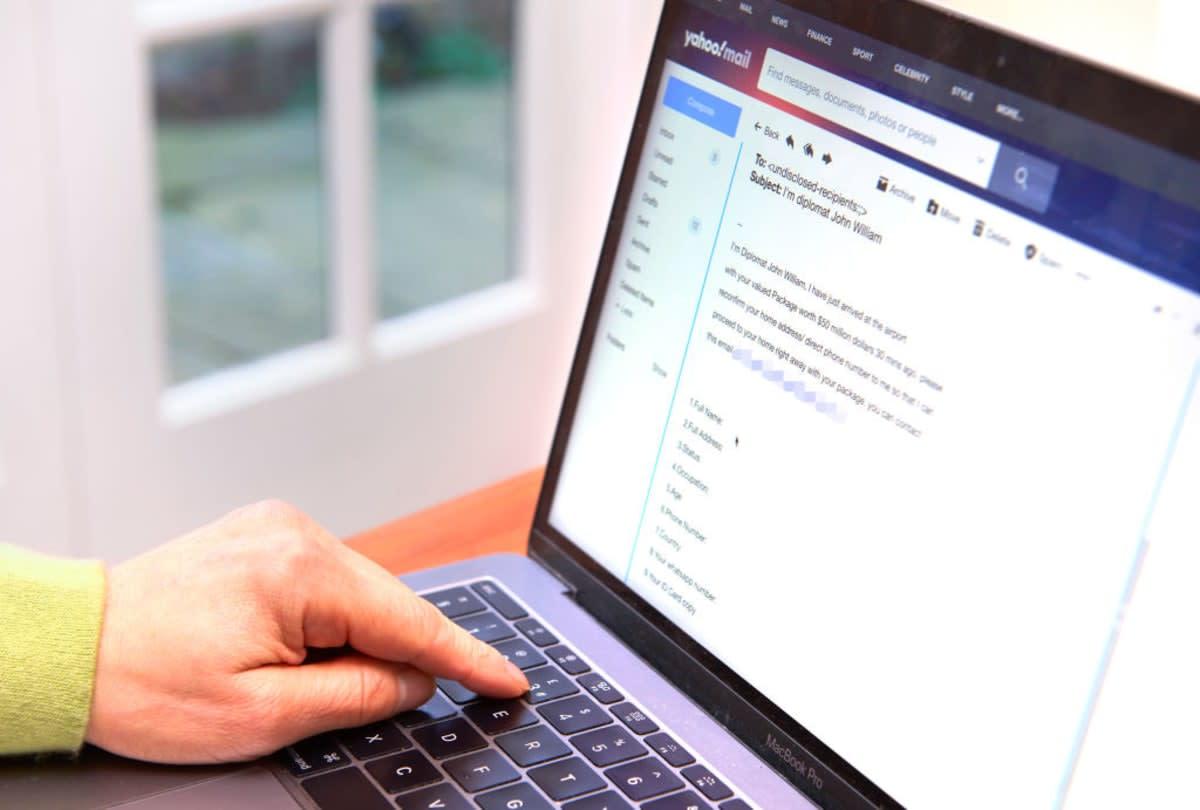

The alarming rise in sophisticated financial scams has put American consumers on high alert. Experts have now warned that fraud is not just prevalent but has triggered a full-blown crisis, with losses exceeding $7 billion in the first three quarters of 2023 alone. This is 5% a rise from the previous year, as reported by the Federal Trade Commission (FTC). Criminals, including organized gangs and transnational entities, are now employing artificial intelligence to pull off voice cloning. This can be highly accurate, and lead to an increase in imposter scams, particularly the grandparent scam. Victims receive calls from fraudsters impersonating a family member and claim to be in dire need of money, often under the pretense of arrest or illness.

1. Grandparent scams - Emotional manipulation

Grandparent scams, exploiting emotional bonds, are increasingly sophisticated in 2024. Scammers, using technology to mimic voices, falsely claim emergencies like arrests or illness, urging secrecy and immediate financial aid. To safeguard against such scams, experts advise against responding to unknown contacts and suggest using a pre-set safe word during emergency calls for verification. Additionally, always double-check unfamiliar requests with known contacts and discuss any unusual financial demands with family members.

2. Romance xcams - Exploiting affection

Romance scams, growing in prevalence, are often orchestrated using social media or dating apps. Scammers form fake romantic bonds, and later fabricate emergencies or financial needs involving illness, jail, or military service, and then ask for money. These scams typically use untraceable payment methods like gift cards and peer-to-peer platforms, says Bankrate's Ted Rossman. A significant portion of financial losses in these scams comes from cryptocurrency transactions. To avoid falling victim, the FTC advises keeping personal and financial information private, discussing new relationships with friends and family, and being skeptical of any requests for money.

3. Cryptocurrency scams - An investment trap

Cryptocurrency scams, leading to over $3.8 billion in losses in 2022, exploit the unregulated nature and lack of legal protections in crypto transactions. These scams often involve false investment opportunities or impersonations of celebrities promising high returns. Scammers also use dating platforms, posing as love interests to lure victims into crypto investments. To avoid these scams, FTC advises never mix online dating with investment decisions, be wary of unsolicited investment advice, and remember that legitimate entities won't demand payments in cryptocurrency.

4. Employment scams - Deceptive opportunities

In an era of increasing layoffs, employment scams are on the rise. Fraudsters use fake job offers and conduct seemingly legitimate interviews to extract personal information or money. They may pose as employers or third-party agencies conducting background checks, only to access victims' bank accounts. Some scams promise easy income in exchange for purchasing a dubious program or involve suspicious financial transactions. To avoid these scams, conduct thorough research on potential employers online, adding terms like “scam” or “review.”

5. Online account tax scams

Scammers are exploiting this need by offering to set up online IRS accounts, using this ruse to file false tax returns and steal refunds. They also leverage this access for broader financial fraud and identity theft. IRS spokesperson Eric Smith warns against trusting third parties who offer to create IRS accounts. Protect yourself by personally setting up your account at IRS.gov, avoiding storing sensitive financial data in emails. If scammed, report immediately to local law enforcement, the FBI, the attorney general, AARP, and the FTC. Most importantly, only initiate tax processes directly through IRS.gov.

Awareness as a shield

According to the FINRA Investor Education Foundation, awareness significantly reduces the risk of falling for scams. Knowing about a specific scam makes individuals 80% less likely to engage with it. The Federal Trade Commission stresses the importance of discussing potential scams with friends and family as a preventive measure. Consumers are urged to exercise caution, verify sources, and protect their personal and financial information to stay safe in the digital age.