A Look at Silver Miners’ 2016 Commodity Exposure

Commodity exposure In the previous part of this series, we looked at miners’ geographic exposure, which is important to consider due to the geopolitical risks some jurisdictions face. It’s equally important to consider their revenue compositions in terms of commodity exposure. Contribution from silver Silver companies are rarely pure-play miners. For investors considering silver […]

March 29 2017, Updated 10:37 a.m. ET

Commodity exposure

In the previous part of this series, we looked at miners’ geographic exposure, which is important to consider due to the geopolitical risks some jurisdictions face. It’s equally important to consider their revenue compositions in terms of commodity exposure.

Contribution from silver

Silver companies are rarely pure-play miners. For investors considering silver stocks due to their leveraged exposure to silver prices, the higher the company’s revenue derived from silver, the better.

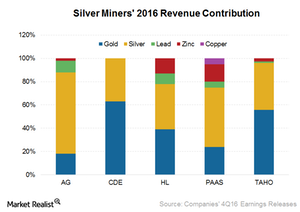

Among the companies we’re considering in this series, First Majestic Silver (AG) derives the highest percentage of its revenue from silver. In 2016, ~70% of its revenue came from silver sales. Pan American Silver (PAAS) also derives the majority of its revenue from silver sales, with ~51% silver revenue. The above graph shows these miners’ commodity exposure in 2016.

Diversifying into gold

In contrast, Coeur Mining (CDE) derived only 37% of its revenue from silver in 2016. Its contribution from silver fell steeply from 53% in 2013 to 37% in 2016, mainly due to the acquisition of the Wharf gold mine in 2016. Hecla Mining’s (HL) proportion of revenue from silver for 2016 was also smaller than that from gold. It derived 39% of its revenue from silver, and 40% came from gold. The rest comes from the sale of lead and zinc.

Tahoe Resources (TAHO) is a primary silver producer. Its flagship mine, Escobal, is mainly a silver mine. With the acquisition of Lake Shore Gold, its weighing toward gold should increase. Tahoe also acquired the Shahuindo project through its acquisition of Rio Alto. This project increases the company’s exposure to gold. In 2016, Tahoe’s revenue contribution from gold was 56%, while from silver, it was 40%.

For investors looking to invest in silver miners, the Global X Silver Miners ETF (SIL) remains one of the leading options. The ProShares Ultra Silver ETF (AGQ), on the other hand, provides leveraged exposure to changes in silver.