Why Home Price Appreciation Differs from State to State

In the judicial states, particularly New York, New Jersey, and Connecticut, we’re seeing much lower home price appreciation.

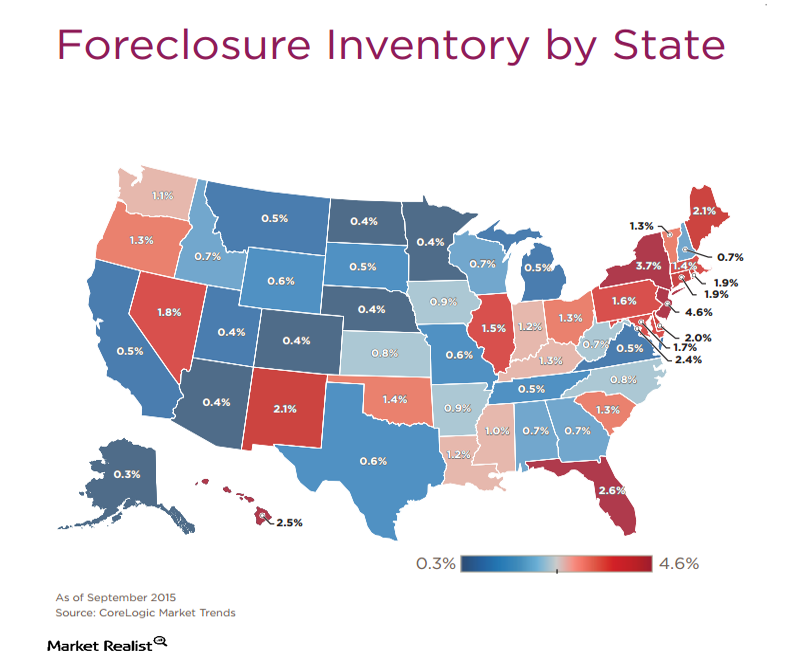

Nov. 13 2015, Updated 5:43 a.m. ET

State foreclosure laws affect foreclosure inventory

There are two basic types of state foreclosure laws: judicial and nonjudicial. In nonjudicial states, foreclosures are handled through a streamlined process and generally take a few months. In judicial states, foreclosures can take years, as judges are often reluctant to push delinquent borrowers out of their homes.

As you can see from the above map, the states with the largest foreclosure inventories—New York, New Jersey, and Florida—have judicial foreclosure processes.

Foreclosure inventory affects home price appreciation

We’ve seen that home price appreciation varies widely by location. In California, the foreclosure pipeline has been worked through, and we’re seeing price appreciation and bidding wars reminiscent of the peak of the bubble years. In the judicial states, particularly New York, New Jersey, and Connecticut, we’re seeing much lower home price appreciation. New York’s foreclosure percentage is 3.7%, while New Jersey’s is 4.6% and Florida’s is 2.6%. Further, there’s very little residential construction, at least compared to construction in some other states.

The problem with much of this inventory is that it is unsellable. In judicial states, many homes sit vacant for years and years, fall into disrepair, and become more expensive to fix than they are worth. This has created blight problems in many localities and is the reason why you see many vacant homes worth $10,000 with a $100,000 mortgage on them. This is depressing prices, especially in areas like the Rust Belt, where vast swaths of cities are vacant.

Implications for mortgage REITs

Real estate prices are a bigger driver for non-agency REITs such as Two Harbors Investment Corp. (TWO) than they are for agency REITs such as Annaly Capital Management (NLY) and American Capital Agency (AGNC). Prices also affect originators such as PennyMac Mortgage Investment Trust (PMT) and Redwood Trust (RWT). Investors interested in trading in the mortgage REIT sector can look at the iShares Mortgage Real Estate ETF (REM).

When prices rise, delinquencies drop. This is important because non-agency REITs face credit risk. For agency REITs that invest in government mortgages, rising real estate prices can drive prepayments, which negatively affect returns.

Rising real estate prices also help reduce stress on the financial system. This makes securitization easier and lowers the cost of borrowing. Finally, REITs with large legacy portfolios of securities from the bubble years are able to stop taking mark-to-market write-downs and may revalue securities upwards.