Why Marriott’s Revenue Increased in 2014

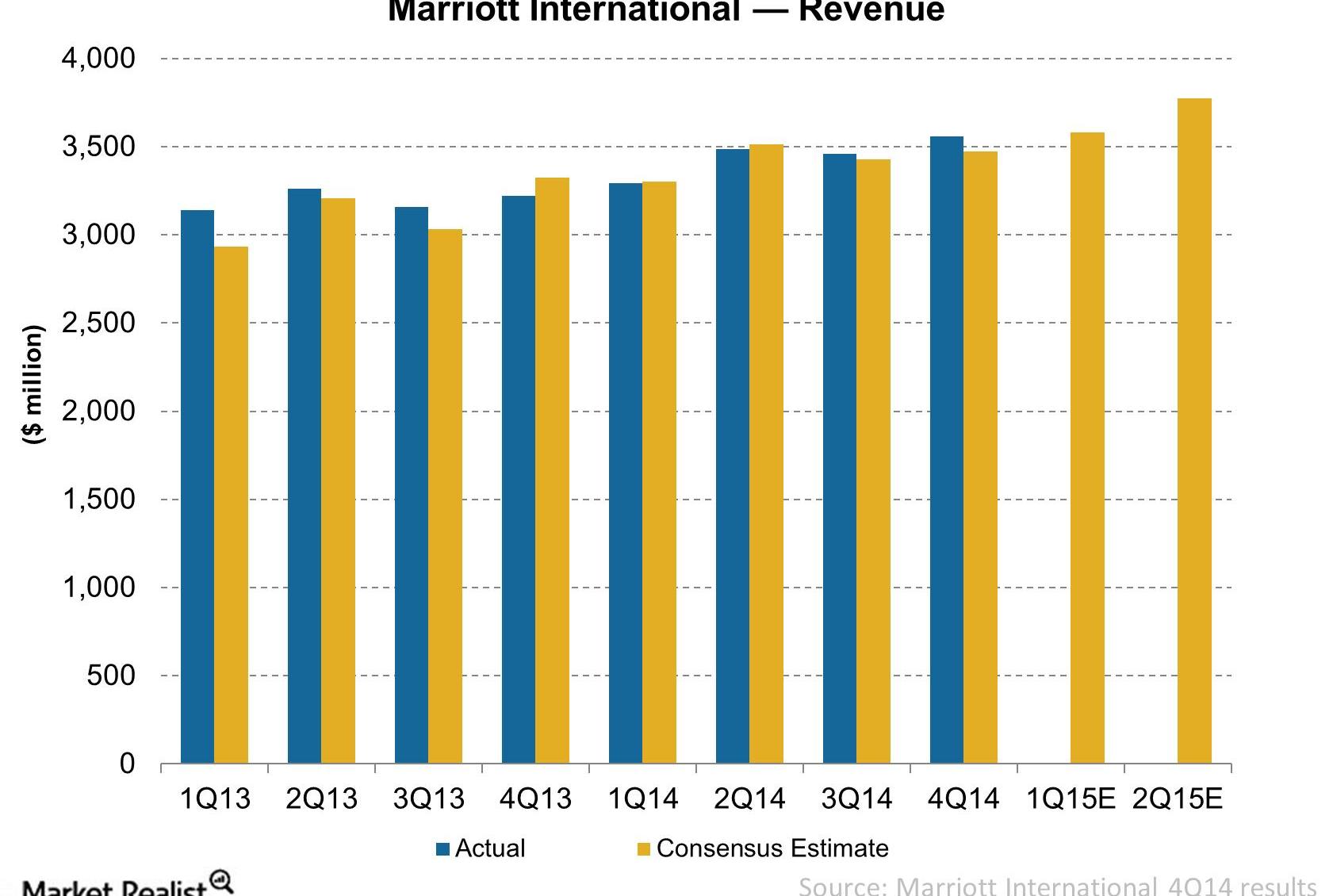

Marriott’s revenues totaled nearly $3.6 billion in the fourth quarter of 2014, compared to $3.2 billion in the fourth quarter of 2013.

March 23 2015, Published 11:18 a.m. ET

Overview of Marriott International

Established in 1927, Marriott International is a global lodging leader, with more than 4,100 properties in 79 countries and territories. Headquartered in Bethesda, Maryland, Marriott reported revenues of nearly $14 billion in fiscal 2014. Marriott (MAR) operates and franchises hotels and licenses vacation ownership resorts under 18 brands.

As of December 31, 2014, the company had ~4,175 lodging properties with 714,765 rooms. These include domestic full-service and limited-service hotels, international hotels, and timeshare properties. To learn more about Marriott, please read Must-know: A company overview of Marriott International Inc.

Marriott International’s main competitors are Hilton Worldwide (HLT), Starwood Hotels & Resorts Worldwide (HOT), Hyatt Hotels (H), and Wyndham Worldwide Corporation (WYN). ETFs like the PowerShares Dynamic Leisure and Entertainment Portfolio ETF (PEJ) and the Consumer Discretionary Select Sector SPDR Fund (XLY) invest in these hotel companies.

4Q14 and 2014 results

On February 18, 2015, Marriott International (MAR) released its 4Q14 and fiscal 2014 results ending in December 2014. Marriott’s fourth quarter fee revenues and its operating profits in 2014 beat consensus estimates. In this part, we’ll discuss Marriott’s revenue.

Marriott’s revenues totaled nearly $3.6 billion in the fourth quarter of 2014, compared to $3.2 billion in the fourth quarter of 2013. Base management and franchise fees totaled $348 million, up 10% year-over-year (or YoY). The increase largely reflected higher revenue per available room (or RevPAR) and new unit growth.

The above chart shows that Marriott’s actual revenues beat consensus estimates by 2.4% in the fourth quarter of 2014. The company’s estimated consensus revenues for 1Q15 and 2Q15 are $3,580 million and $3,772 million, respectively.

Series overview

In this series, we’ll discuss Marriott’s 4Q14 and fiscal 2014 earnings, as well as its guidance for 2015. We’ll also discuss Marriott’s room pipeline, premium valuation, outlook for the future, and share buybacks.