All You Need to Know about Real Estate Private Equity

Real estate private equity funds have been attracting unprecedented amounts of capital, with assets under management reaching an all-time high of $724 billion.

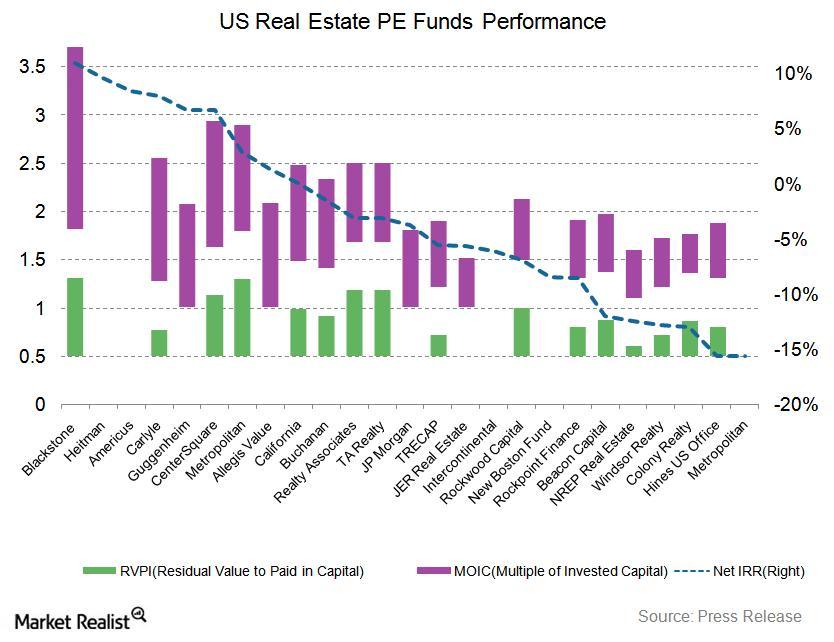

May 18 2015, Published 4:39 p.m. ET

What makes real estate private equity attractive?

Real estate private equity funds have been attracting unprecedented amounts of capital with assets under management (or AUM) reaching an all-time high of $724 billion. One of the key drivers of this growth is an increase in real estate valuations, which has led to a significant rise in the value of portfolios held by fund managers. Private equities (or PEs) primarily focus on superior risk-adjusted yields. The main objectives of private equities are the attraction of capital, sourcing and qualifying investment opportunities, fund and investment structuring, and exit strategies.

Private real estate funds have seen an average increase in NAV (net asset value) for 17 straight quarters, thus generating annualized returns of 17% over the past three years. Their activity has direct ramifications on passive strategies employed by REITS and other publicly traded real estate firms such as Toll Brothers (TOL) and ETFs such as the Vanguard REIT Index ETF (VNQ) and the iShares US Real Estate ETF (IYR).

Private equity investing is not easily accessible for the ordinary investor. Most private equity houses typically look for investors who are willing to commit as much as $25 million. Although some firms have dropped their minimums to $250,000, this is still out of reach for most people. However, tracking trends in this industry serves as an invaluable indicator to assess investors’ real estate allocation in their equity portfolios, in addition to helping answer the question of whether to gain access through direct ownership of real estate or via a passive strategy through publicly traded assets.

Unlike direct buying, where an investment can appreciate significantly within a year, one’s real estate PE portfolio will appreciate only after two to three years due to the “J-Curve.” Realty PE funds typically have tenure of five to eight years. Some PE players fund only final-stage liquidity gaps. The tenure of such funds is shorter than that of the development-based funds. Shorter tenure is also common among rental-based funds.

Understanding the J-curve

IRRs (internal rate of return) are typically negative in the first few years of a fund’s life, but they increase over time as funds are exited and then stabilize in the final years of the fund’s life. IRRs following this trend form a J-Curve trajectory.

The chart above shows the median net IRR at each quarter for funds of 2004-2011, illustrating the impact of the downturn on funds of 2005-2007 vintage years. Median IRRs of vintage 2007 funds underwent a significant decline that began in June 2008, with the net IRR reaching a low of -41.8% in March 2009. However, the median IRR for funds of this vintage has since had a steady recovery, standing at 3.9% as of June 2014. 2005 and 2006 vintage funds, which would have invested the majority of their capital at peak pricing, have not seen the same level of recovery.

PE funds do not take all of your money at one go, but ask you to release the amount in tranches as they find new investment opportunities. At the end of the term, the funds sell their investments in the secondary market and return the money to the investors. Some of the liquid ETFs that also invest in real estate are the CBL & Associates Properties (CBL) and the Pennsylvania Real Estate Investment Trust (PEI).