Why Minimum Volatility Funds Have Outperformed

Minimum volatility funds have outperformed broader markets in the long term. By limiting the downside during the troughs of a volatile market, the minimum volatility index is better able to capitalize on rebounds.

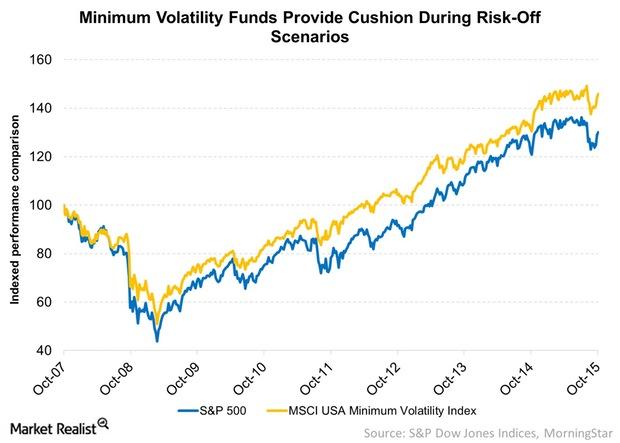

Nov. 4 2015, Updated 12:04 a.m. ET

2. Go min vol.

If you want broad market exposure with potentially less risk, minimum volatility ETFs might be a good fit. These funds seek to track market indexes with a mix of historically less volatile stocks, so you can still invest in global, US, developed international and emerging markets with potentially fewer bumps in the road.

Market Realist – Minimum volatility funds have outperformed broader markets in the long term.

Minimum volatility ETFs track indices that seek to capture the broad equity market with a reduced amount of volatility. These indices seek to provide better risk-adjusted returns and protect against the downside risks that occur in the market every now and then.

When volatility (VXX)(VIXY) is rising, broader equity markets have typically faltered, as there’s a lot of fear in the market. When the broader equity markets fall, the minimum volatility ETFs act as a cushion. However, as volatility falls, the broader markets outperform the ETFs.

Perhaps surprisingly, though, minimum volatility indices have outperformed the S&P 500 (RSP) in the long term. The iShares MSCI USA Minimum Volatility Index (USMV) has actually outperformed the S&P 500 Index (RSP) over the last ten years. By limiting the downside during the troughs of a volatile market, the minimum volatility index is better able to capitalize on rebounds, as the graph above shows.

For example, let’s say an index starts a year at 100. Let’s say it falls by 20% that year, which brings it down to 80. Let’s say it gains 20% in the following year. This would take the index only to (80+(80*20/100)), which is 96. Let’s assume that the minimum volatility-sibling of that index also started at 100 and, for illustration sake, captures 50% of the upside and downside of the standard index. In the first year, it would lose only 10% of its value, bringing it down to 90. In the second year, it would gain 10%, taking it up to 99. So it’s better able to capitalize on a rebound.

The minimum volatility indices, which track emerging market (EEMV) stocks, give you less volatile access to emerging markets.