Why capacity utilization is an important economic indicator

Capacity utilization rates are approaching long-term historical averages.

Nov. 20 2020, Updated 1:14 p.m. ET

Higher utilization and inflation rates

Most people don’t think industrial data affects office real estate investment trusts (or REITs). However, it does influence the top-line growth of commercial REITs like SL Green Realty Corporation (SLG). Higher utilization rates can be an inflation driver because more expensive capacity is used, which can push rent higher.

Capacity utilization is a bellwether of economic activity

Capacity utilization is a good top-down macroeconomic indicator that helps forecast the labor market, final demand, consumption, and inflation. While manufacturing is no longer the primary driver of the U.S. economy, it still influences the economy to a large degree—particularly for unskilled workers. Recently, U.S. manufacturing has been undergoing a bit of a renaissance because of cheap energy prices. There’s still a difference between wages overseas and wages here, but low natural gas prices are offsetting that difference. Also, as wages rise overseas, the cheap labor arbitrage (taking advantage of lower wages) is fading away. The Fukushima nuclear disaster also showed how long supply chains are vulnerable.

An increase in capacity utilization generally signals an increase in employment and capital spending. Lower-skilled workers have struggled since the financial crisis, which dampened demand and consumption. Things are finally starting to improve. Construction jobs are rebounding and more companies starting to move toward onshore production. Increased capital spending is a big economic driver too. For a long time, corporations have been in a maintenance mode towards capital spending.

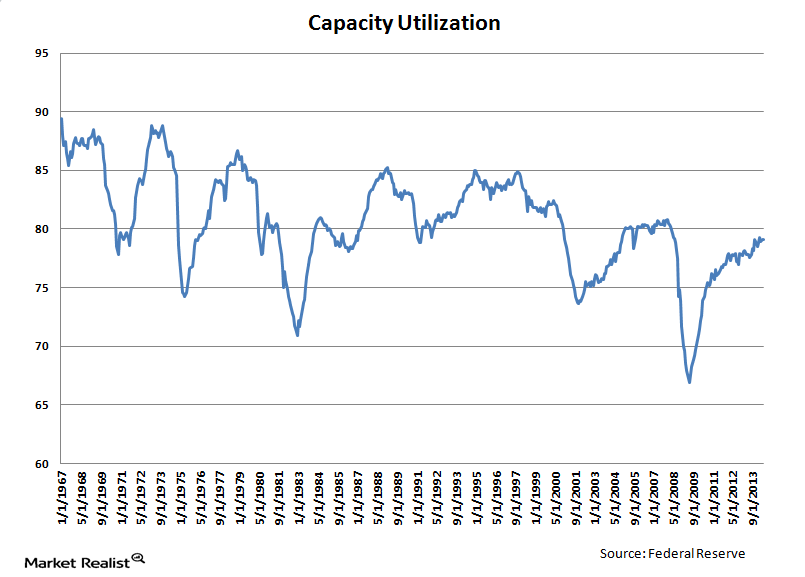

Capacity utilization rates are approaching long-term historical averages

Capacity utilization was 79.1% in June, flat with May. Capacity utilization has risen steadily since the economy bottomed in 2009. Over the past year, it has risen 130 basis points.

From 1972 to 2012, capacity utilization averaged 80.2%. It was highest in the early 1970s, peaking at around 89%. It bottomed at 66.9% in 2009. This suggests there’s a lot of room for production to expand before we start feeling inflation pressures. High capacity utilization levels in the 1970s were a big cause of inflation.

Impact on commercial REITs

Industrial production and capacity utilization are numbers that get a lot of focus from the Fed. These figures not only help forecast economic activity, but also impact inflation. Once the Fed believes inflation is too low, the outlook will change. The Fed certainly will be happy to see capacity utilization approaching long-term historical averages.

While inflation is completely under control, the Fed will look at capacity utilization when formulating the policy. Right now, the only economic statistic that really matters is unemployment—everything else is secondary. The days of quantitative easing are numbered, but low short-term interest rates will be here for at least another year or two.

Interest rates are an important input for the commercial REIT sector. They tend to be leveraged, and they are trade based on their dividend yields. Increases in interest rates may not be welcome news for office REITs like Brookfield Office Properties (BPO), SL Green (SLG), Vornado Realty Trust (VNO), Kilroy Realty Corporation (KRC), and Highwoods Property (HIW). But, the reason for the increase is good news—higher capacity utilization signals stronger economic growth, which is an important driver of rental income and vacancy rates.