Syd Leibovitch on the Tax Law Trapping California Homeowners

Rodeo Realty founder Syd Leibovitch believes a decades-old capital gains exclusion tax provision is discouraging many longtime homeowners from selling.

July 17 2026, Published 1:47 p.m. ET

California's housing affordability crisis is often blamed on rising interest rates, insufficient new construction, and a lack of available inventory. But according to Rodeo Realty founder Syd Leibovitch, another factor is really the culprit and receives far less attention: federal tax law.

Leibovitch believes a decades-old capital gains exclusion tax provision is discouraging many longtime homeowners from selling, reducing the number of homes available across virtually every price point.

We spoke with Leibovitch about why he believes tax policy has become an overlooked contributor to America’s housing shortage and affordability concerns. He believes that this is the single reason that prices are rising at the exorbitant clip that we have seen in recent years.

Q: Most discussions about housing affordability focus on inventory. Why do you think inventory remains so low?

Most people immediately point to a lack of new construction, and that's absolutely not the real problem. The real issue is tax law. We have a large number of homeowners who would like to move up, downsize, relocate, be closer to family, move to retirement communities, etc., but they are financially trapped because of the tax consequences of selling.

Q: What specifically in the tax code is creating that problem?

Leibovitch: Prior to 1997, someone could sell their home and buy another of equal or greater value and defer their gain, essentially pay no tax. I had so many clients who used this. They would buy their starter home. As their family grew and they moved up in their jobs, they bought a larger home. Some moved a third time due to school districts to avoid the cost of private school when they felt another area would be better for their kids. When their kids graduated High School, they moved again to an area more conducive to the life of “empty nesters.” When they had grandchildren, many moved again to be nearby. When they no longer felt comfortable living on their own, they moved to retirement communities. Most people cannot do that now. They are stuck in their homes.

This is because the Tax Relief Act of 1997 eliminated the IRS 1034 section, allowing you to defer your gain, which was replaced with IRC section 121, which allows someone to sell their primary residence if they lived in it for two out of the last five years and get $250,000 in gain for an individual and $500,000 for a married taxpayer filing together tax-free.

That exclusion amount has not changed in almost thirty years. If you calculate that amount just based on inflation, $500,000 is the same as $1,050,000 today. If you use both U.S. home appreciation numbers based on the published median price by year, $500,000 would be equal to $1,800,000 and $2.5 million in California.

Q: Can you give me an example?

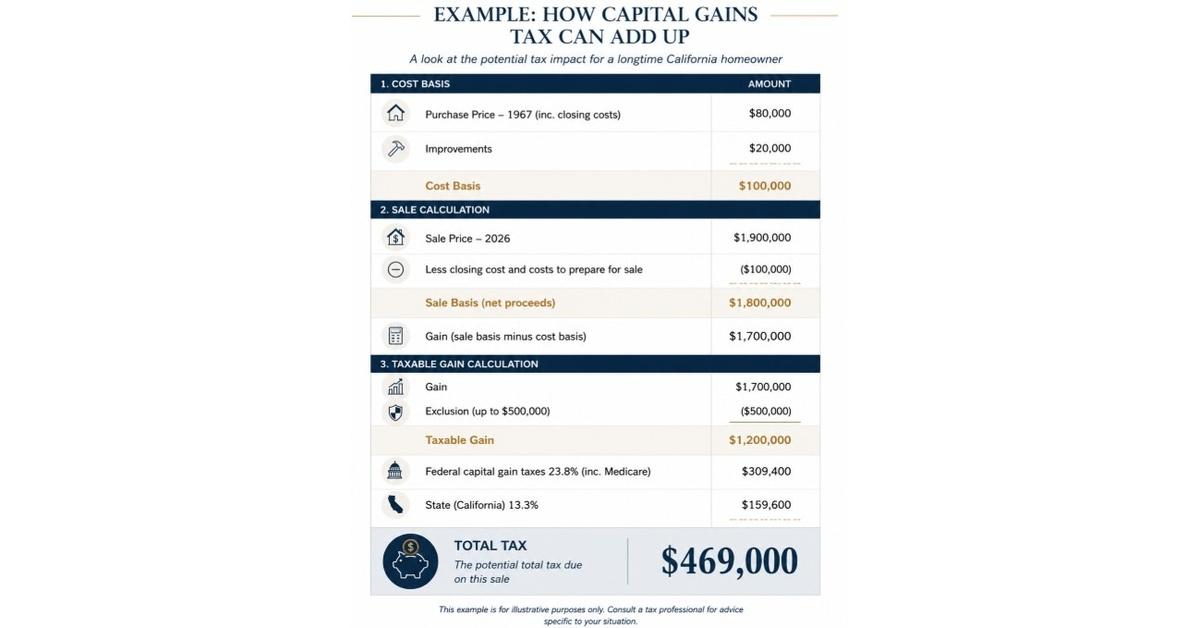

Leibovitch: Yes. My parents do not want to sell their home, but let’s use them as an example. They bought their home in 1967. It was about $80,000. Over the years, maybe they have spent $20,000 in improvements. Therefore, their cost basis is about $100,000. Their home would sell for about $1,900,000. Assuming after closing costs, commissions, etc., they end up with a sale basis of $1,800,000. Next, you subtract the sale basis from the cost basis, which leaves you a gain of $1,700,000

When someone in this scenario finds out that it will cost them almost $500,000 to sell their home, they don’t. There is a step-up when the first spouse passes away, and there will essentially be no tax. Do we really want people to feel trapped in their home and not be able to sell until one of them dies?

Is it fair for someone who lived in their home for 60-years to get an exclusion that is no larger than someone who lived in their home for just 2-years?

Q: How does that affect homeowner behavior

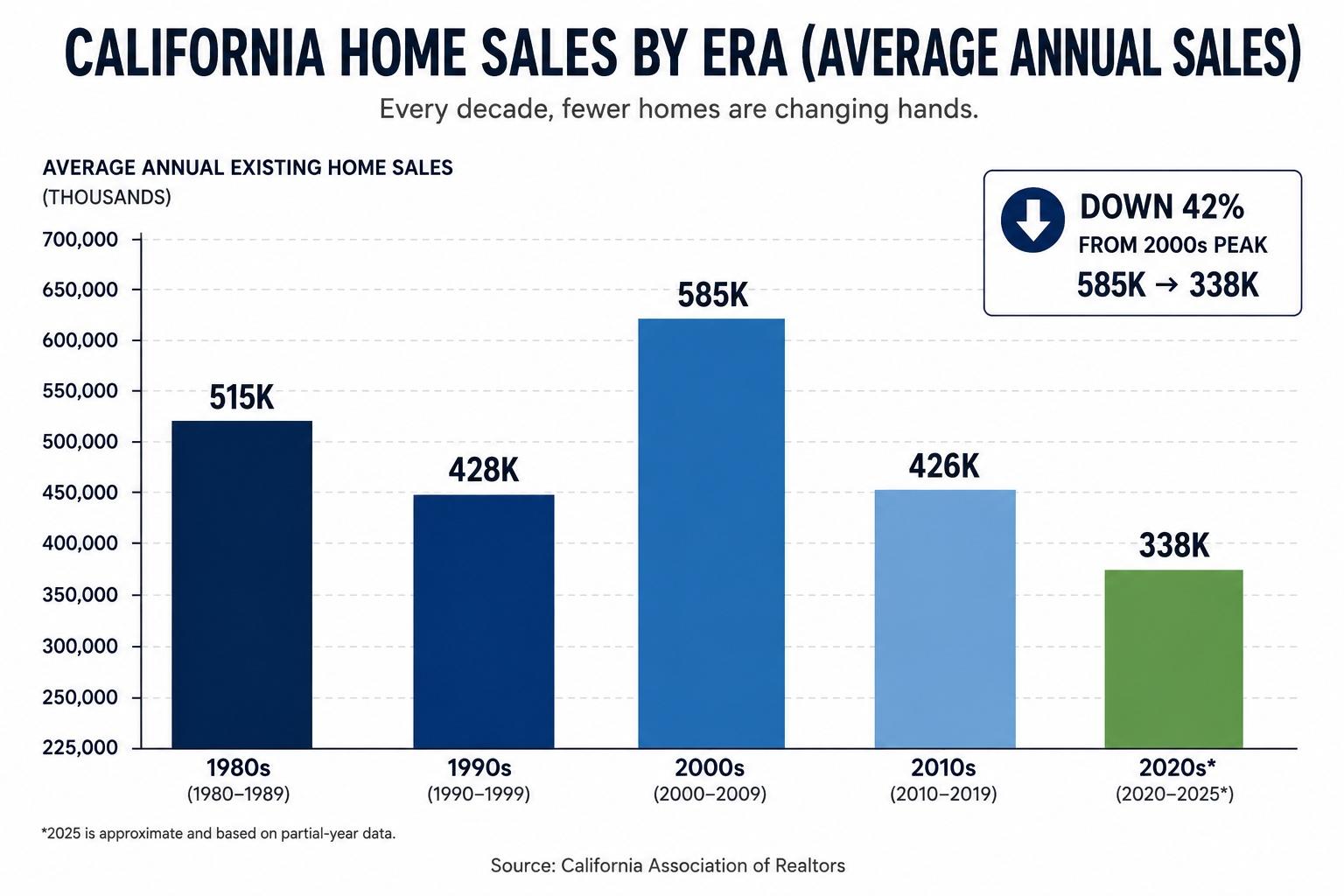

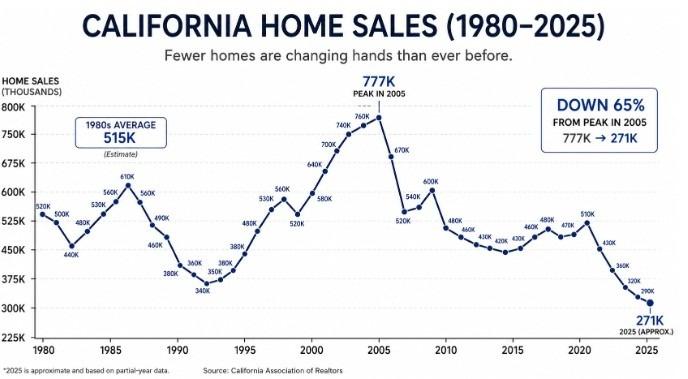

Leibovitch: Prior to 1997, data from the National and California Association of Realtors showed that people moved about every 7 years on average. It's over 20 years today! People are stuck in their homes and waiting to die to sell. This is where I point to new construction.Since 1990, there have been 3.6 million new housing units added, yet the number of sales has dropped consistently. This includes 2017-2022, where we saw the lowest interest rates since the early 1970s, so you can’t blame rates!

We see it all the time. Someone purchased a home decades ago for a relatively modest amount. Today, that property may be worth several million dollars. Once they calculate their taxable gain and potential tax liability, many decide not to sell.They may no longer need the home. Their children may have moved away. They may want to relocate or downsize. But after seeing the tax bill, they decided to stay put.

Q: Why does that matter for the broader housing market?

Leibovitch: Because housing works like a chain reaction.When someone doesn't sell their $3 million home, that home isn't available for the person looking to move up from a $1.5 million home. If they can’t find a home, they may not sell that home. Then the person looking to move up from a $750,000 home can’t buy the $1.5 million home and so on. The effects ripple through every segment of the market to where people don’t sell. It’s just like everything else. Its supply and demand. If fewer people sell, prices are pushed up.

People often think housing shortages only affect entry-level buyers, but inventory constraints impact every price range.

Q: Some would argue these homeowners have still made substantial profits. Why should policymakers be concerned?

Leibovitch: Because this isn't just about one homeowner's gain. It's about market mobility.Healthy housing markets depend on people being able to move when their circumstances change. When a tax policy discourages movement, fewer homes become available. Fewer homes for sale mean more competition. More competition pushes prices higher.Ultimately, buyers pay the price.

Q: Is this only affecting luxury homeowners?

Leibovitch: No.Years ago, this was primarily an issue for higher-value properties. Today we're seeing it affect middle-class homeowners as well. Home values have risen so much in many California communities that even owners of relatively modest homes are facing significant tax consequences when they sell.That's something very few people anticipated when the exclusion limits were established.

Q: What would happen if the law were changed?

Leibovitch: More homes would come onto the market almost immediately.Not only are people not selling which freezes the market all the way down, there is a tremendous amount of shadow inventory. I would estimate there are hundreds of thousands of homes sitting vacant where people are waiting for their spouse or parent to pass away to avoid a huge tax liability. They don’t want to be landlords, and they can no longer live in their home. Its just a failure of government to have let this go on so long.

Most housing policy proposals take years to have a measurable effect. New construction takes time. Regulatory changes take time. But if homeowners felt they could sell without facing such a large tax burden, many who have been postponing a move would finally list their homes.

Bringing back the 1034 would have an immediate impact. In fact, I believe it will lower prices in the short term, but once this mess from bad tax law corrects itself, we will see a much more stable and less dysfunctional housing market.